You Saved. You Planned. You Did Everything Right…

Now the College System Is Punishing You For It.

Why are families like yours being asked to pay $80,000/year…

while others pay $30K or less for the same degree?

See how to protect your savings and cut your net cost.

- Find money colleges don’t advertise

- Lower your net cost (not just the sticker price)

- Leave with a simple next-step plan

There’s a Playbook.

Colleges Use It Against You.

Most families think college pricing is based on income alone.

It’s not.

Colleges use a pricing system to decide who pays more, who gets help, and who gets pushed into the Funding Gap.

I call that system CollegeBound Economics™.

Most families think college pricing is about income.

It's not!

Colleges look at far more than income when they decide what your family will pay.

That’s why two families who look similar on paper can get very different results.

And that’s how families get pushed into the Funding Gap.

Reported Results

These are the average 4-year savings families reported after grants and scholarships lowered their real college cost.

Public Colleges

$34,480*

Average 4-year savings

(856 students)

Private Colleges

$107,983*

Average 4-year savings

(812 students)

All Colleges

$70,262*

Average 4-year savings

(1,668 students)

*Results vary by student and college. See FTC Disclosure below.

Want to see what this looks like for your family? Join the free workshop.

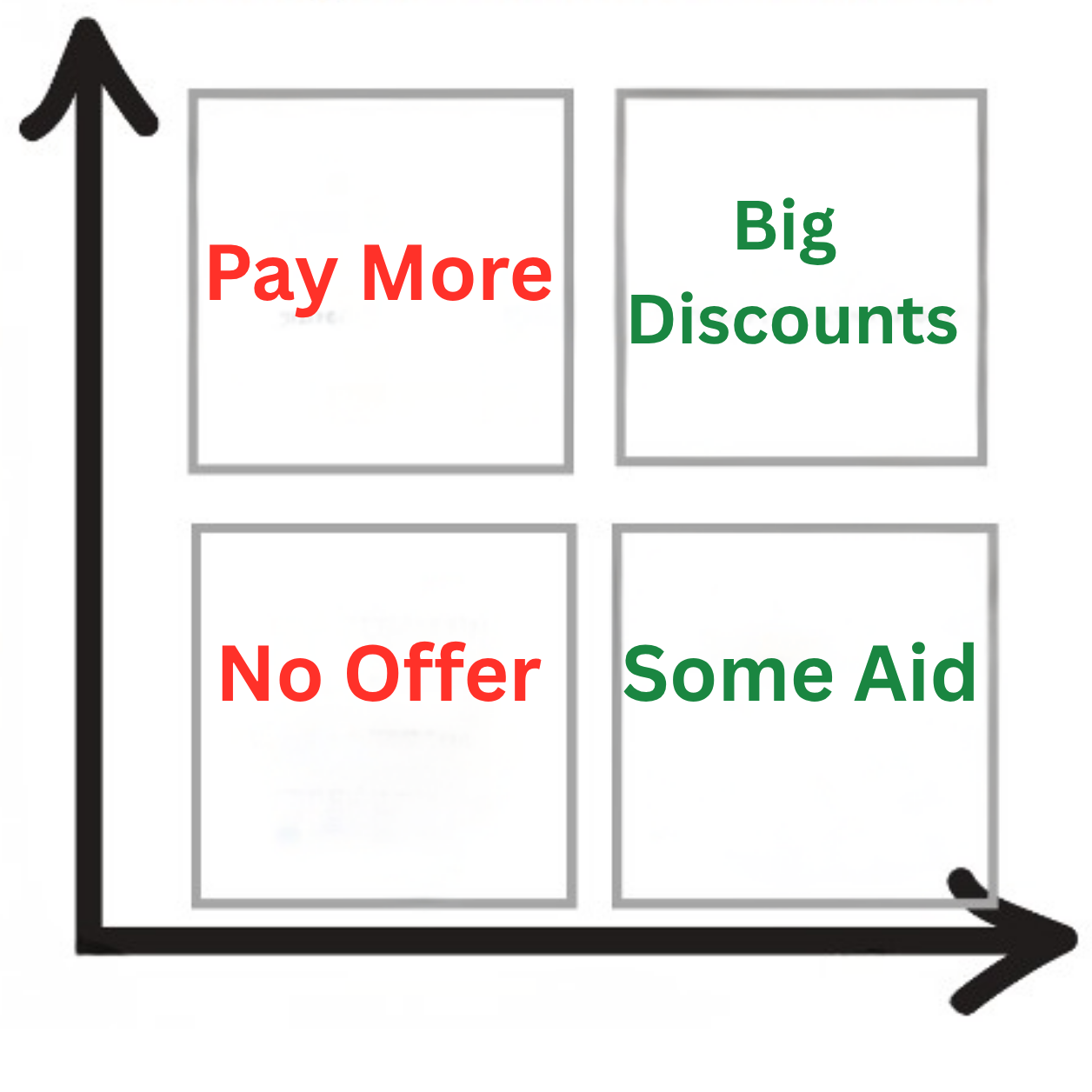

Are You in the "College Funding Gap?"

Too “rich” for aid. Not rich enough to write $80K checks.

-

Many families earning $100K–$400K get squeezed here

-

You make too much for most need-based aid

-

Paying $30K–$90K/year can wreck retirement

Here’s the fix — watch this quick video:

The 3-Step Process That Helps Families Pay Less

So you can cut net cost without draining retirement.

Step 1:

Academic Modeling

Find the schools that will pay your student.

We show you how to spot real merit money fast.

Outcome: $20k–$40k per year in scholarships

Step 2:

Financial Aid Modeling

Increase aid — legally.

Learn how schools count income + assets, and what you can do about it.

Outcome: $10k–$30k per year in additional aid

Step 3:

Retirement Preservation

Lower costs without touching retirement.

Use the right mix of school choice + timing + aid strategy.

Outcome: Retirement stays on track

Real Families, Real Savings

Three quick case studies showing how families lowered their real college cost.

Case Study #1: Julie

A private college ended up costing less than community college and State U.

Case Study #2: Sarah

Sarah negotiated for more aid at a private college and brought her final net cost down to about the same as in-state.

Case Study #3: The Lampert Family

The Lampert family cut the cost of expensive private colleges by 58%.

Watch the 3 case studies ->

See how real families lowered college costs by thousands.

Join the free workshop and see what this could look like for your family.:

What You’ll Learn in This Free Workshop

Cut your net cost without draining retirement.

- Why "sticker price" is not what most families pay

- Where schools hide grant and scholarship money

- The FAFSA/CSS mistakes that quietly raise your cost

- How to protect savings, assets, and 529s

- A simple next-step plan based on your family’s numbers

Colleges Are Targeting Your Wallet!

-- as reported May 2025 in the New York Times

If your family earns $150K or more, you might feel stuck—too "rich" for aid, too smart to overpay.

Now, it’s confirmed: The New York Times reports colleges are profiling families like yours before you even apply.

They’re not just reviewing applications; they’re using algorithms to decide what to charge your family.

Watch Now ->

Meet Peter Lampert

CPA, Tax Attorney, Fiduciary Financial Advisor, and College Affordability Specialist who’s helped 34,000+ families save $70,262* on average using legal strategies colleges hope you never learn

What parents say after the workshop

Real feedback from real families.